Navigating the world of car ownership can sometimes present unexpected twists and turns. Perhaps you’re in a situation where you need to part with your vehicle but still owe money on the loan, or maybe you’ve found a great deal on a car where the current owner wants someone else to assume their payments. In either scenario, understanding the crucial role of a well-drafted take over car loan payments contract template is absolutely essential for a smooth and legally sound transaction.

This process, often referred to as a loan assumption or a private sale involving existing debt, isn’t as simple as a handshake. It involves significant financial and legal implications for both the original borrower (seller) and the new borrower (buyer). For the seller, it could mean relief from monthly payments and potentially an improvement in their debt-to-income ratio. For the buyer, it can offer an opportunity to acquire a vehicle without needing to secure an entirely new loan, sometimes even at a better interest rate or with more favorable terms if the original loan was advantageous.

However, without a clear and legally binding agreement, both parties are exposed to considerable risks. Misunderstandings about responsibilities, payment schedules, or even the condition of the vehicle can lead to disputes, damage to credit scores, and potential legal battles. That’s why having a robust template that outlines every aspect of the agreement is not just recommended, it’s practically a necessity.

Navigating the Process of Taking Over Car Loan Payments

The idea of transferring car loan payments might seem straightforward on the surface, but in practice, it’s quite complex and rarely a direct transfer without the original lender’s involvement. Most auto loans are not directly assumable, meaning the lender typically does not allow one person to simply step into another’s shoes on the existing loan agreement without a formal application and approval process.

From the seller’s perspective, their primary goal is usually to be completely released from financial responsibility for the vehicle. This is critical because even if a buyer agrees to make payments, if the loan remains in the seller’s name, any missed payments by the buyer will negatively impact the seller’s credit score and could lead to repossession actions against the seller. Protecting one’s credit is paramount in this type of transaction.

For the buyer, taking over payments can seem appealing as it might bypass the initial credit checks and down payment requirements of a new loan. However, the buyer is also assuming the full responsibility for the debt, often without the same consumer protections that come with purchasing from a dealership or securing a brand-new loan. It’s vital for the buyer to understand the full terms of the existing loan, including interest rates, remaining balance, and any potential penalties.

The role of the lender cannot be overstated. In most cases, the lender will need to approve the new borrower. This often involves the buyer applying for the loan in their own name, either through a refinance or a novation agreement, where the original contract is effectively replaced with a new one involving the new borrower. In some rare instances, a lender might allow a simple assumption, but this is far from common in the auto loan industry.

If the lender does not allow a direct assumption, the most common legal ways to achieve this transfer involve the buyer obtaining their own loan to pay off the seller’s existing loan, or the buyer entering into a “loan assumption” or “transfer of ownership” agreement directly with the seller that still legally holds the seller responsible for the initial debt unless a specific release of liability is granted by the lender. A truly effective arrangement for the seller will always include a formal “release of liability” document from the original lender, freeing them from all future financial obligations related to the car loan.

Without lender approval for a direct transfer or a new loan by the buyer, any private agreement between the buyer and seller acts as a personal contract, but the original loan still ties the seller to the lender. This is why a well-structured agreement, even for the private arrangement, is crucial. It defines the obligations between buyer and seller, even if it doesn’t immediately remove the seller’s name from the original loan.

Key Elements of Your Agreement

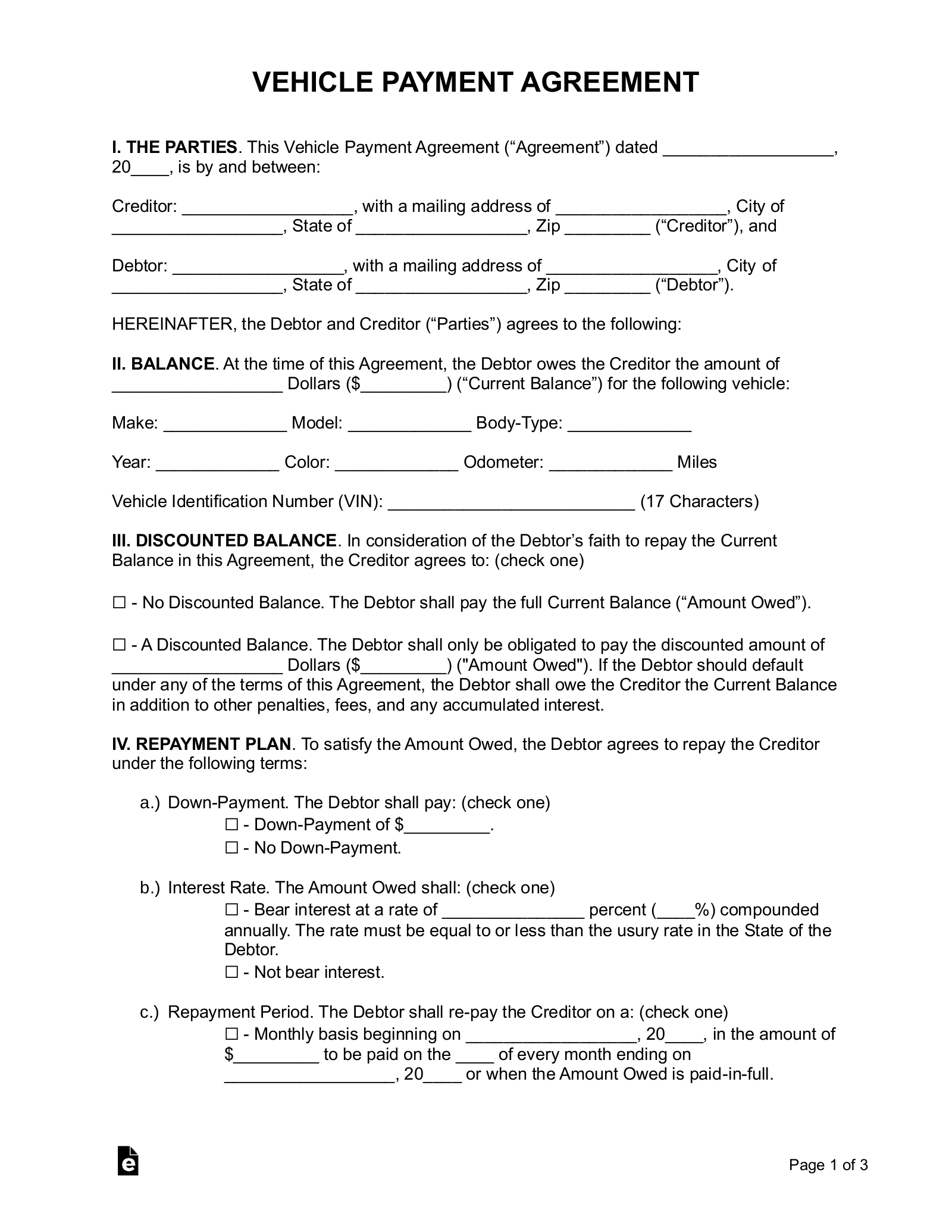

Whether it’s a direct assumption (if the lender permits) or a private arrangement where the buyer takes on the payment responsibility while the seller remains the official borrower, the contract needs to be comprehensive. It should include the full legal names and addresses of both parties, detailed vehicle identification information (VIN, make, model, year, mileage), the exact outstanding loan balance, the lender’s name and loan account number, and a precise schedule of payments. Furthermore, it should specify who is responsible for insurance, maintenance, and any late payment fees. Crucially, the agreement must clearly state the date of transfer of possession and responsibility, an indemnity clause to protect the seller in case of buyer default, and provisions for what happens if the buyer defaults on payments. It’s also wise to include clauses regarding vehicle condition and any agreed-upon inspection results.

Why a Solid Contract Template is Non-Negotiable

When you’re dealing with significant financial obligations like a car loan, relying on verbal agreements or informal notes is a recipe for disaster. A comprehensive contract template provides a clear roadmap for both parties, detailing expectations and responsibilities in an unambiguous manner. It serves as a legal document that can be referenced or enforced if any disputes arise down the line, protecting both the buyer and the seller from potential future headaches.

Without a formal agreement, misunderstandings are almost inevitable. Imagine a scenario where the buyer misses a payment, leading to a late fee. Who is responsible for that fee? What if the car gets into an accident before the title is officially transferred? Who covers the deductible or repairs? These are just some of the questions that a properly designed take over car loan payments contract template addresses, preventing ambiguity and ensuring that both parties know exactly where they stand.

Ultimately, using a specialized template ensures that all critical legal and financial aspects are considered and documented. This structured approach helps in achieving a transparent and fair transaction, minimizing risks for everyone involved. It doesn’t just outline the terms; it legally binds the parties to them, offering peace of mind.

- Ensures legal compliance and validity of the agreement.

- Clearly defines roles, responsibilities, and financial obligations for both buyer and seller.

- Provides a clear, written record of all terms agreed upon, preventing disputes.

- Protects both parties by outlining remedies in case of breach or default.

- Streamlines the transfer process by making sure all necessary details are addressed.

Engaging in a transaction to take over car loan payments requires meticulous attention to detail and an unwavering commitment to formal documentation. While the allure of a quick deal might be strong, cutting corners on the legal framework can lead to significant financial and credit damage for both the buyer and the seller. A thorough, well-understood agreement is the bedrock of a successful transfer, ensuring clarity and protecting the interests of everyone involved.

Therefore, whether you are looking to offload a vehicle with an existing loan or eager to acquire one by assuming its payments, investing time in understanding and utilizing a proper contract is an investment in your financial security and peace of mind. Always remember that open communication, due diligence, and a legally sound document are your best allies in navigating these complex waters successfully.