Facing a loan default can be a challenging situation for both creditors and debtors. When a borrower fails to meet their financial obligations, creditors may need to consider repossession of collateral. A crucial step in this process is issuing a formal notice, and having a reliable notice of repossession letter template is essential for legal compliance and clear communication.

This article will guide you through the intricacies of creating and utilizing such a notice. We’ll explore the legal requirements, the key components of an effective letter, and provide a comprehensive sample. Understanding these elements ensures you protect your rights as a creditor while adhering to all necessary regulations.

By the end of this guide, you will be well-equipped to draft a professional and legally sound repossession notice. This knowledge is vital for any entity dealing with secured loans and potential defaults, helping to streamline the process and mitigate future legal complications.

Understanding The Legal Framework For Repossession Notices

The act of repossession is governed by specific state and federal laws designed to protect both creditors and debtors. These laws dictate the procedures creditors must follow, including the requirement to send a formal repossession notice. Failure to comply can lead to legal challenges, fines, or even the invalidation of the repossession itself.

Many jurisdictions mandate that debtors receive a “right to cure” notice before repossession. This notice provides a window for the debtor to bring their loan current, thus avoiding the loss of their collateral. The specific timeframe and requirements for this type of notice can vary significantly by state, so thorough research is crucial.

Creditors must also be aware of rules regarding the sale of repossessed property. After repossession, many states require creditors to send a “notice of intent to sell” or a “notice of private sale” to the debtor. This informs the debtor about the planned disposition of the collateral and their right to redeem the property before sale.

State-Specific Repossession Regulations

Repossession laws are not uniform across the United States; they vary considerably from state to state. For instance, some states require a court order before repossession of certain types of property, while others allow self-help repossession under specific conditions. It is imperative to consult with legal counsel to understand the specific statutes in your operating state.

Key areas where state laws often differ include:

- The required waiting period after a default before repossession can occur.

- Specific language and disclosures that must be included in any repossession notice.

- Rules regarding what constitutes a proper notification method (e.g., certified mail, personal delivery).

- Debtor’s rights after repossession, such as the right to redeem the property.

Debtor Rights And Creditor Responsibilities

Even in cases of default, debtors retain certain rights throughout the repossession process. Creditors have a responsibility to respect these rights and conduct the repossession lawfully and ethically. This includes avoiding breaches of the peace during repossession and providing clear, timely notices.

After repossession, creditors typically have a duty to sell the repossessed property in a “commercially reasonable manner.” This means obtaining a fair market price for the collateral to minimize any potential deficiency balance owed by the debtor. Documenting all steps of the process is crucial for demonstrating compliance.

Furthermore, if the sale of the collateral does not cover the full outstanding debt, the debtor may still owe a “deficiency balance.” Creditors must send a deficiency notice to the debtor, explaining the amount owed and how it was calculated. A well-crafted notice of repossession letter template can set the stage for these subsequent communications.

Crafting A Compliant Repossession Notification

An effective repossession notice goes beyond merely informing the debtor of the action. It serves as a legal document that sets the stage for the subsequent steps of the repossession process. Ensuring accuracy and completeness in this notice is paramount to avoid legal challenges down the line.

The language used should be clear, concise, and easy for an 8th-grade reading level to understand. Avoid legal jargon where plain English suffices. This clarity helps prevent misunderstandings and demonstrates good faith on the part of the creditor.

Using a standardized notice of repossession letter template helps maintain consistency and ensures all critical information is included. This reduces the risk of overlooking a required legal disclosure. Customizing the template for each specific situation is also essential.

Essential Components Of A Repossession Letter

Every repossession notice should include several critical pieces of information. These elements ensure the debtor is fully informed and that the creditor meets their legal obligations. Missing any of these details could jeopardize the creditor’s position.

Here are the vital components:

- Date of Notice: Clearly states when the letter was issued.

- Debtor’s Name and Contact Information: Ensures the letter is sent to the correct party.

- Creditor’s Name and Contact Information: Identifies the sender.

- Account Number/Loan ID: Helps both parties easily identify the specific defaulted loan.

- Description of Collateral: A precise description of the repossessed item (e.g., vehicle make, model, VIN).

- Date and Time of Repossession: Specifies when the property was taken.

- Location of Repossessed Property: Informs the debtor where their property is being stored.

- Reason for Repossession: Clearly states the default event (e.g., missed payments, breach of contract).

- Outstanding Balance: The amount currently owed on the loan.

- Instructions for Redemption: Explains how the debtor can get their property back, including payment amount and deadline.

- Notice of Intent to Sell: Informs the debtor that the property will be sold if not redeemed.

- Contact Person/Department: Provides a point of contact for debtor inquiries.

- Legal Disclaimers: Any state-specific legal language required.

Tips For Sending The Notice Effectively

Beyond the content, the method of sending the repossession notice is equally important. Creditors must ensure proof of delivery to demonstrate that the debtor received the notice. This can be critical evidence in any subsequent legal dispute.

Best practices for sending the notice include:

- Certified Mail with Return Receipt: Provides undeniable proof that the letter was sent and received.

- First-Class Mail: Often sent in conjunction with certified mail as a backup.

- Personal Delivery: In some cases, personal delivery might be an option, but ensure proper documentation.

- Electronic Communication: If agreed upon in the loan contract, electronic notices may be permissible, but always check state laws.

- Maintain Records: Keep copies of the sent letter, proof of mailing, and any correspondence related to the notice.

Consistency in the mailing address is also vital. Always use the most current address on file for the debtor. If the debtor has moved without notifying the creditor, it may complicate the notification process, but efforts to locate them are often required.

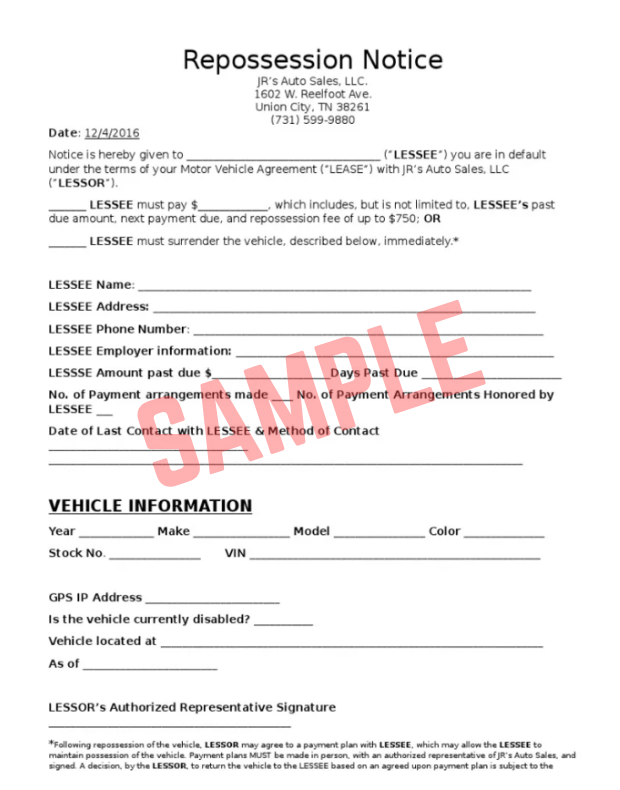

Sample Notice Of Repossession Letter Template

Below is a comprehensive sample of a notice of repossession letter template. This example includes the necessary details and structure to inform a debtor of a vehicle repossession. Remember to adapt this template to your specific situation and state’s legal requirements. This sample should be reviewed by legal counsel before use.

[Your Company Letterhead]

[Date]

[Debtor’s Full Name]

[Debtor’s Address]

[City, State, Zip Code]

Subject: Notice of Repossession – Account No. [Account Number]

Dear [Debtor’s Full Name],

This letter serves as a formal notice that the collateral securing your loan account number [Account Number] has been repossessed. The repossession occurred on [Date of Repossession] at approximately [Time of Repossession]. This action was taken due to your default on the terms of your loan agreement dated [Date of Loan Agreement], specifically for [Reason for Repossession, e.g., failure to make required payments].

The repossessed collateral is described as follows:

- Year: [Vehicle Year]

- Make: [Vehicle Make]

- Model: [Vehicle Model]

- Vehicle Identification Number (VIN): [VIN]

- License Plate Number: [License Plate Number]

The collateral is currently being stored at:

[Storage Facility Name, if applicable]

[Storage Facility Address]

[City, State, Zip Code]

You may contact [Storage Facility Phone Number, if applicable] to arrange for the retrieval of any personal property not affixed to the vehicle.

As of the date of this letter, the outstanding balance on your loan account is $[Outstanding Balance]. This amount includes the principal, accrued interest, and any late fees or repossession costs incurred to date.

You have the right to redeem the repossessed collateral. To redeem the collateral, you must pay the full outstanding balance of $[Outstanding Balance], plus any additional costs and fees that may accrue, including storage and preparation for sale costs, by [Redemption Deadline Date – often 10-21 days after notice]. Payment must be made in certified funds (cashier’s check or money order) to our office at [Your Company Address]. Please contact [Contact Person/Department] at [Phone Number] to confirm the exact redemption amount and to arrange for redemption.

Please be advised that if the collateral is not redeemed by the deadline mentioned above, we intend to sell the collateral. The sale will be conducted in a commercially reasonable manner. This may be a private sale or a public auction. You will be notified separately of the specific details of any planned sale. If the proceeds from the sale are less than the amount you owe on your loan, you may still be responsible for paying the remaining balance, known as a deficiency balance. Conversely, if the sale proceeds exceed the amount you owe, you may be entitled to the surplus.

We encourage you to contact us immediately to discuss your options. You may reach [Contact Person/Department] at [Phone Number] during business hours [Business Hours].

Sincerely,

[Your Name/Company Representative Name]

[Your Title]

[Your Company Name]

[Your Company Phone Number]

[Your Company Email Address]

Navigating the complexities of loan defaults and repossessions requires careful attention to legal details and clear communication. Utilizing a well-structured notice of repossession letter template is a critical tool for creditors. It not only ensures compliance with state and federal laws but also provides a clear, documented record of the actions taken.

By understanding the legal framework, meticulously crafting your notices, and maintaining thorough records, you can manage the repossession process effectively. This diligence helps protect your interests as a creditor and fosters transparency in challenging financial situations. Always remember to consult with legal professionals to ensure your specific procedures align with current regulations.